Find Independent Insurance Options With Confidence: A Complete Guide

Shopping for insurance doesn't have to be confusing. In this guide, we break down how independent insurance agents work, why they're different from captive agents, and how they can save you time, stress, and money — at no extra cost to you. Whether you're comparing home, auto, or business coverage, learn what to look for in an agent, the right questions to ask, and how to spot red flags. Plus, we weigh independent agents against buying direct online so you can make the choice that's right for your situation. Get the clear, no-pressure guidance you need to find coverage that truly fits your life.

2/24/2026

Shopping for insurance can feel overwhelming. Between the jargon-filled policies, the endless fine print, and the pressure to make a quick decision, it's easy to feel like you're navigating a maze without a map. You want good coverage at a fair price, but how do you know you're making the right choice?

Here's the short version: working with an independent insurance agent can cut through the confusion. Unlike agents who represent just one company, independent agents shop multiple carriers to find coverage that actually fits your needs. They work for you, not the insurance company.

At Silver Harbor Insurance, we believe in laying out your options so you can decide with confidence. No pressure, no gimmicks. Just clear guidance and independent options from carriers we trust. Let's break down what independent agents do, why they matter, and how to find one who will truly have your back.

What is an independent insurance agent?

An independent insurance agent is a licensed professional who works with multiple insurance companies rather than just one. Think of them as your personal shopper for insurance. While a captive agent (like one who works exclusively for State Farm or Allstate) can only sell you their company's products, an independent agent can compare policies from several carriers to find the best match for your situation.

Most independent agencies are small, locally owned businesses. Many are family operations that have served their communities for decades. When you call an independent agency, you're likely reaching someone who lives in your neighborhood, shops at the same grocery stores, and understands the unique risks of your area.

The key distinction is who they work for. Captive agents represent the insurance company. Independent agents represent you. They have access to quotes from multiple carriers, which means they can prioritize your needs over pushing a specific company's products. We work with a variety of respected carriers to give our clients options that fit their specific situations.

Independent agents don't charge you extra for this service. Their commission comes from the insurance company whose policy you choose, not from your pocket. So you get comparison shopping, personalized advice, and ongoing support at no additional cost.

Why choose an independent agent?

The benefits of working with an independent agent go beyond simply having more options. Here's what sets them apart.

Access to multiple insurance carriers

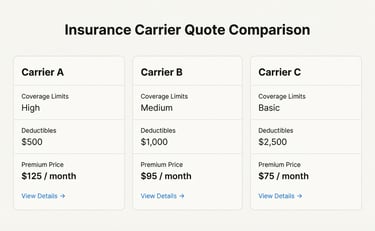

When you request a quote from a single company, you get one option. When you work with an independent agent, you might see quotes from 5, 10, or even 15 different carriers. This matters because insurance companies evaluate risk differently. One company might offer better rates for drivers with clean records, while another might be more competitive for homeowners in certain zip codes.

Your independent agent does the legwork of gathering these quotes and presenting them in a way that's easy to compare. They can explain why one policy costs more than another and what you're getting (or not getting) for that difference in price. This transparency helps you make an informed decision rather than guessing whether you're getting a good deal.

Personalized service and local expertise

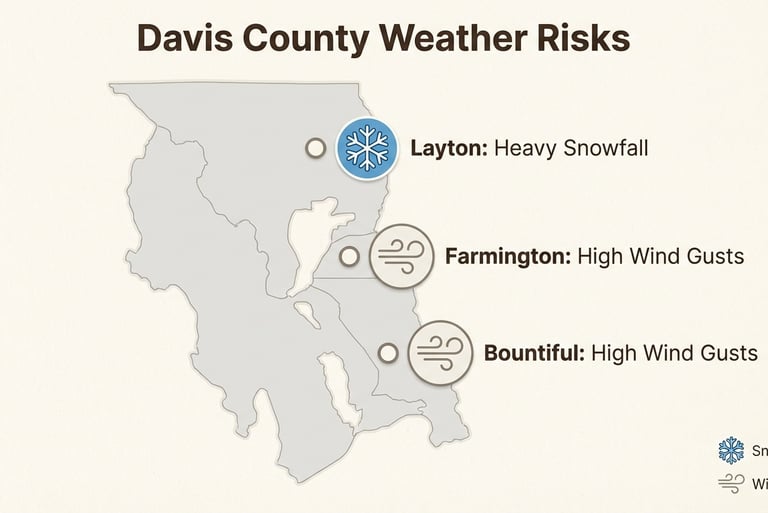

Independent agents live and work in the communities they serve. A local agent in Davis County understands risks that a call center in another state might miss. They know about Utah's winter weather patterns, the specific flood risks in certain neighborhoods, and how local building codes affect replacement costs.

This local knowledge translates into better coverage recommendations. For example, an agent familiar with Utah's minimum car insurance requirements can make sure you're not just meeting the legal minimums but actually protecting yourself adequately. They can also spot gaps in your coverage that you might not have considered, like water backup protection or ordinance coverage for older homes.

Claims advocacy

Perhaps the most valuable benefit of an independent agent shows up when you actually need to use your insurance. Filing a claim can be stressful, especially after a car accident, house fire, or other disruptive event. Your independent agent acts as your advocate throughout the process.

They can help you understand what your policy covers, assist with the paperwork, and communicate with the insurance company on your behalf. If there's a dispute about coverage, your agent knows the policy language and can argue for your interests. This support can make a significant difference in both the outcome of your claim and your peace of mind during a difficult time.

One-stop shopping

Most independent agencies offer a full range of insurance products: home, auto, life, business, umbrella, and specialty coverage. This means you can handle all your insurance needs through a single point of contact. Your agent can coordinate coverage across policies to eliminate gaps and redundancies, and you only need to remember one phone number when you have questions.

How to find the right independent agent

Not all independent agents are the same. Here's how to evaluate your options and find someone who will truly serve your interests.

Check credentials and licensing

Start by verifying that any agent you're considering is properly licensed in Utah. You can check licensing status through the Utah Insurance Department's website. While you're at it, look for professional designations like CIC (Certified Insurance Counselor) or CPCU (Chartered Property Casualty Underwriter), which indicate additional training and expertise.

It's also worth asking which carriers the agent represents. A good independent agent should work with a variety of reputable companies, not just one or two. This variety ensures they can actually shop around for you rather than steering you toward a limited set of options.

Ask the right questions

Before committing to an agent, have a conversation about how they work. Here are some questions worth asking:

Which insurance carriers do you work with?

How do you handle claims support?

What's your process for reviewing coverage?

How often will we review my policies?

What's the best way to reach you when I have questions?

Pay attention to how they answer. A good agent will welcome these questions and give you clear, straightforward responses. They should be willing to explain coverage options in plain English, not industry jargon.

Look for red flags

Be wary of agents who use high-pressure sales tactics or try to rush you into a decision. Insurance is a significant purchase that affects your financial security. You should never feel pushed to sign before you're ready.

Other warning signs include agents who seem to push one carrier exclusively, can't clearly explain how commissions work, or struggle to answer basic questions about coverage details. Transparency is essential in this relationship. If an agent won't give you straight answers, find someone who will.

Consider local vs. national

While some independent agencies are part of larger networks, there's real value in working with a truly local agent who knows Davis County. Local agents understand the specific risks and requirements of your area. They've built relationships with local contractors, know which carriers have the best claims service in your community, and can provide the kind of personalized attention that national operations struggle to match.

If you're ready to explore your options, you can start a request with us anytime. We serve families and businesses throughout Davis County, including Layton, Farmington, Kaysville, Bountiful, and surrounding areas.

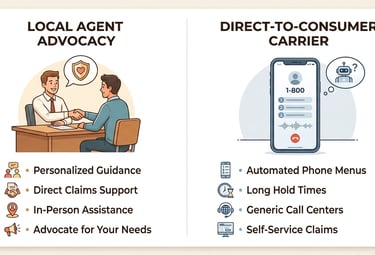

Independent agent vs. buying direct online

You've probably seen the ads promising to save you hundreds on insurance in just a few minutes. These direct-to-consumer options have their place, but they're not right for everyone. Here's how to think about the trade-offs.

When an independent agent makes sense

An independent agent is usually the better choice if you have complex insurance needs, multiple policies to coordinate, or if you value having a personal relationship with someone who knows your situation. If you own a home, run a business, or have significant assets to protect, the guidance of an experienced agent can help you avoid costly coverage gaps.

An agent also adds value if you want ongoing service. Your insurance needs change over time. A good agent will review your coverage annually and make recommendations as your life evolves. When you buy direct online, that ongoing relationship typically doesn't exist.

When direct online might work

Buying insurance online can make sense for very straightforward situations. If you're a renter with minimal possessions, a single person with one car and no home, or someone who's comfortable managing your own policies, the convenience of online purchasing might outweigh the benefits of an agent relationship.

Online options also tend to work better for people who are primarily price-focused and don't anticipate needing much support. If you're confident you understand what you're buying and won't have questions later, going direct can be a reasonable choice.

The cost question

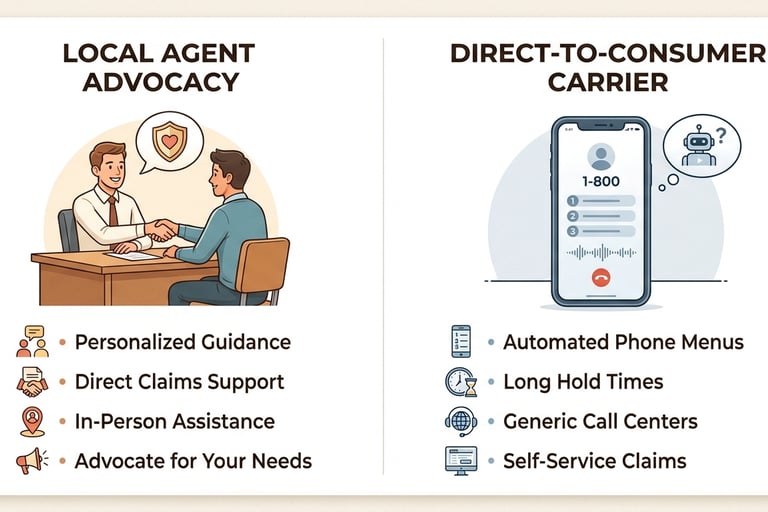

Here's something the online ads don't always make clear: independent agents don't charge you extra. Their commission is built into the premium whether you use an agent or not. When you buy direct, the insurance company keeps that commission instead of paying it to an agent. You're not necessarily saving money by cutting out the middleman.

What you are giving up is advocacy and service. When you have a question or need to file a claim, you'll be calling a 1-800 number and talking to whoever answers. With an independent agent, you're calling someone who knows your name and your policy.

What to expect when working with an independent agent

If you've never worked with an independent agent before, here's what the process typically looks like.

The relationship starts with a conversation. A good agent will ask about your assets, your risks, your budget, and your priorities. They want to understand not just what you need to insure, but what you're trying to protect. This conversation helps them identify coverage options that match your actual situation rather than selling you a generic policy.

Next, they'll gather quotes from multiple carriers. When they present these options, they should explain the differences in coverage, not just the differences in price. Sometimes the cheapest option leaves you exposed to significant risks. Understanding what's covered and what's not is essential to making a good decision.

Once you choose a policy, the agent handles the paperwork and makes sure your coverage starts when you need it. But their role doesn't end there. A good agent provides ongoing service, including annual policy reviews, assistance with claims, and updates to your coverage as your life changes.

Making your decision with confidence

Finding the right insurance coverage is about more than just price. It's about having confidence that you're protected when something goes wrong. Independent agents earn that confidence by giving you choices, explaining your options in plain English, and standing by you when you need help.

The key is finding an agent who puts your interests first. Look for someone who's transparent, knowledgeable, and genuinely interested in understanding your needs. Ask questions, trust your instincts, and don't settle for high-pressure sales tactics.

At Silver Harbor Insurance, we believe the decision should always be yours. We lay out your options so you can decide with confidence. No pressure, no gimmicks. Just trusted protection, simplified.

Ready to explore your options? Give us a call at (801) 332-9888 or reach out through our website. We're here to help you find the coverage that fits your life.

Frequently Asked Questions

How do I find independent insurance options with confidence near me?

Start by asking friends and neighbors for recommendations. Check online reviews, verify licensing through your state insurance department, and interview potential agents before committing. A good local agent will welcome your questions and provide clear answers about their process and the carriers they represent.

What should I look for when trying to find independent insurance options with confidence?

Look for an agent who takes time to understand your needs, explains coverage in plain English, and represents multiple reputable carriers. Check their licensing status, ask about their claims support process, and make sure you feel comfortable with their communication style before making a decision.

Does it cost more to find independent insurance options with confidence through an agent?

No. Independent agents don't charge extra fees to consumers. Their commission comes from the insurance company, not your pocket. The price you pay for a policy is typically the same whether you buy through an agent or direct from the company.

How many carriers should an independent agent represent to help me find independent insurance options with confidence?

There's no magic number, but a good independent agent should work with at least 5-10 different carriers. This variety ensures they can actually shop around for you and find competitive options. Ask potential agents which carriers they work with and why.

Can I find independent insurance options with confidence for both home and auto coverage?

Yes. Most independent agents offer a full range of insurance products, including home, auto, life, and business coverage. This one-stop shopping approach makes it easier to coordinate your coverage and manage all your policies through a single point of contact.

What's the difference between an independent agent and a broker when I want to find independent insurance options with confidence?

Independent agents and brokers both work with multiple carriers, but brokers typically charge fees for their services while agents earn commission from the insurance companies. For most personal insurance needs, an independent agent provides the same access to multiple carriers without additional cost to you.

A Quick Note: We write these articles to help you navigate the complex world of insurance, but they do not replace the expertise of a licensed agent. View this content as a starting point rather than a final word on your specific policy needs. Always talk to a professional to ensure you carry the right protection.

Contact

Quote and support requests 24/7

Phone

© 2026. All rights reserved.