Utah Minimum Car Insurance Requirements (2026): 30/65/25 Explained + $3,000 PIP

Utah’s minimum auto insurance is 30/65/25 plus $3,000 PIP. Learn what the numbers mean, when minimums fall short, and what to consider instead.

AUTO INSURANCE

2/5/2026

Utah Minimum Car Insurance Requirements in 2026 (And What 30/65/25 Really Means)

If you drive in Utah, you’re required to carry minimum auto insurance—and as of policies issued or renewed on/after January 1, 2025, the liability minimum is 30/65/25, plus Personal Injury Protection (PIP) that includes at least $3,000 per person for medical expenses.

Quick answer

Utah’s minimum required auto insurance is typically 30/65/25 in liability coverage, plus PIP with at least $3,000 per person for medical expenses.

30/65/25 helps pay for other people’s injuries and property damage when you’re at fault.

PIP ($3,000 minimum medical per person) helps pay your/your passengers’ medical costs first in many situations.

Minimum limits may meet the legal requirement, but they can be tight in real-world accidents—especially with injuries or multiple vehicles.

Next step: If you want to sanity-check your current limits, you can Request a Quote or Talk to an Agent.

What you’ll learn

Utah’s required minimum coverages (and what’s optional vs. waived)

What 30/65/25 actually pays for

Why minimum limits can run out faster than most people expect

Utah minimum auto insurance requirements (what you must carry)

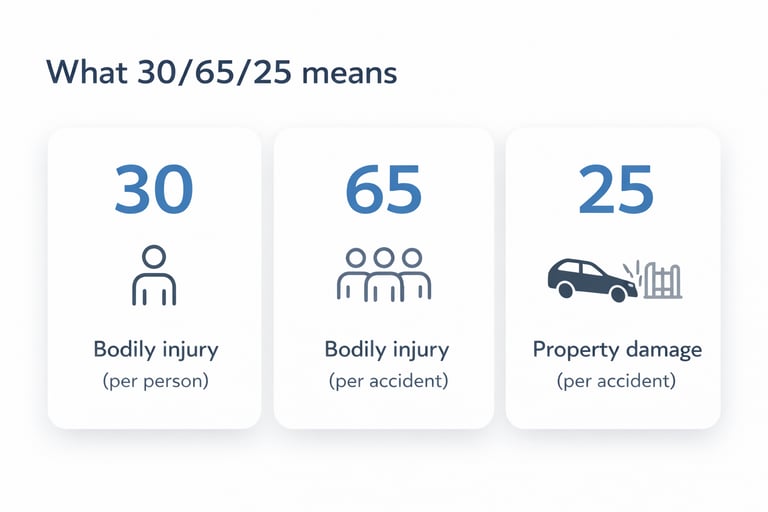

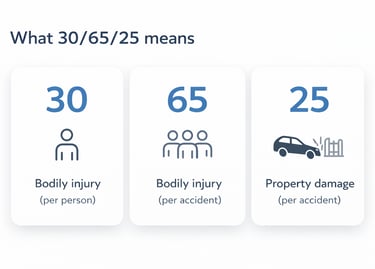

1) Liability coverage: 30/65/25

Utah law sets minimum liability limits for policies issued or renewed on/after January 1, 2025 as:

$30,000 bodily injury liability per person

$65,000 bodily injury liability per accident (total for everyone injured)

$25,000 property damage liability per accident

2) Personal Injury Protection (PIP): includes at least $3,000 per person for medical

Utah PIP minimum benefits include:

Up to at least $3,000 per person for necessary medical-related expenses (medical, hospital, rehab, etc.)

Lost income benefit (subject to limits)

Household services benefit (subject to limits)

Funeral/burial benefit up to $1,500

Death benefit payable to heirs $3,000

Utah’s consumer guidance often describes this as: the first $3,000 in medical expenses are covered by your PIP before you can pursue the at-fault driver’s insurer for those medical bills.

3) Uninsured and underinsured motorist coverage (UM/UIM): typically included unless waived

Utah’s “owner’s or operator’s security” generally includes:

Liability coverage

Uninsured motorist coverage (UM) unless affirmatively waived

Underinsured motorist coverage (UIM) unless affirmatively waived

PIP (with some vehicle-type exceptions)

What does 30/65/25 mean (in plain English)?

Think of 30/65/25 as three separate “caps” on what your policy will pay for damage you cause to others:

30 = Bodily Injury (BI) per person

The most the policy will pay for injuries to one person you hurt in an at-fault accident.65 = Bodily Injury (BI) per accident

The most the policy will pay for injuries to everyone combined in that one accident.25 = Property Damage (PD) per accident

The most the policy will pay for other people’s property you damage in that accident (vehicles, fences, buildings, etc.).

Important: Your liability limits don’t pay to repair your own car—that’s typically collision (optional) and comprehensive (optional).

Is Utah’s minimum coverage “enough” in real life?

Minimums are designed to meet the legal requirement—not to guarantee you’re fully protected in every accident.

Here’s what industry data shows about how fast costs can add up:

Claim statistics: injuries can land right on the minimum limit

According to ISO/Triple-I data, the average bodily injury liability claim in 2024 was $28,278, and the average property damage liability claim was $6,770.

That matters because Utah’s minimum is $30,000 per injured person. So the “average” injury claim leaves only:

$30,000 − $28,278 = $1,722 of cushion (per person)

And if more than one person is injured, the $65,000 per accident cap becomes the next pressure point:

2 average injury claims: $28,278 × 2 = $56,556 (only $8,444 left under $65,000)

3 average injury claims: $28,278 × 3 = $84,834 (that’s $19,834 over the $65,000 cap)

Bottom line: You don’t need a “worst-case” crash for minimum limits to feel tight—especially with multiple injured people.

What happens if you don’t carry enough insurance?

If you’re at fault and damages exceed your limits, your insurer typically pays up to your policy limit—and the remaining amount may become your responsibility. What happens next can vary, but commonly includes:

The injured party may pursue you for the unpaid amount (often through negotiation or a lawsuit)

You may have to pay out of pocket over time, use savings, or deal with a court judgment (this can impact wages/assets depending on your situation)

This is general information—not legal advice—and outcomes depend on the facts of the claim.

What happens if you drive without insurance in Utah?

Utah requires you to maintain “owner’s or operator’s security” and to carry proof/evidence when operating a vehicle.

If you drive without required security, Utah law describes it as a class C misdemeanor with minimum fines of:

$400 first offense

$1,000 second/subsequent offense within three years

Utah also ties insurance to registration and proof requirements.

So what limits do most people choose instead of the minimum?

There’s no one-size-fits-all number, but many drivers consider stepping up from minimums when they:

Have savings/assets they want to protect

Drive frequently (commuting, rides with family, carpools)

Carry passengers often

Want more cushion for multi-vehicle or multi-injury accidents

Common higher-limit benchmarks people compare:

100/300/100 (more breathing room for injuries + property damage)

250/500/100 (for higher asset protection needs)

Umbrella liability (adds extra liability protection above auto/home, typically in $1M increments—availability varies)

A licensed agent can help match limits to your situation and budget.

Quick checklist: how to decide if minimum limits are right for you

Consider increasing limits if:

You’d struggle to write a check for $10,000+ unexpectedly

You regularly drive in heavy traffic corridors

You frequently have passengers in your vehicle

You own a home or have growing savings/income

Ready to review your Utah auto limits?

Your coverage. Your call. We lay out your options so you can decide with confidence. No gimmicks, no push—just principled guidance and a decision you control.

Requests 24/7 — Responses within 1 business day

What to have ready (helps us answer fast):

Current policy declarations page (if you have it)

Driver names + dates of birth

Vehicle year/make/model/VIN (if available)

Your preferred limits (or “show me a few options”)

A Quick Note: We write these articles to help you navigate the complex world of insurance, but they do not replace the expertise of a licensed agent. View this content as a starting point rather than a final word on your specific policy needs. Always talk to a professional to ensure you carry the right protection.

Contact

Quote and support requests 24/7

Phone

© 2026. All rights reserved.