What Home Damage Is Usually Covered by Homeowners Insurance (And What Usually Isn’t)

See what home damage is usually covered by homeowners insurance (fire, wind, theft, burst pipes) vs usually not covered (flood, wear and tear, gradual leaks, pests). Includes common gray areas and a quick policy checklist.

HOMEOWNERS INSURANCE

2/11/2026

Homeowners insurance typically covers sudden, accidental damage caused by common covered perils—like fire, wind/hail, theft, vandalism, falling objects, or a burst pipe—subject to your deductible, limits, exclusions, and endorsements.

Your policy form and endorsements can change what’s covered (many homeowners have an HO-3-style policy, but details vary)

“Sudden and accidental” is often the line between covered vs. not covered

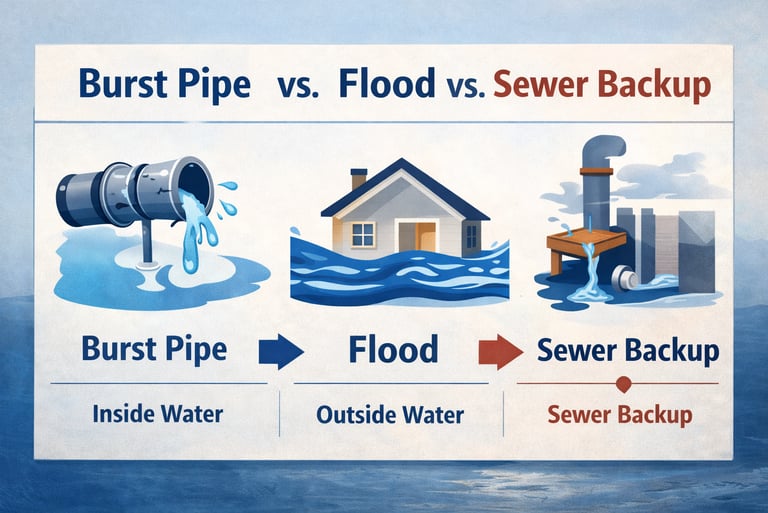

Water is the most confusing category: burst pipe ≠ flood ≠ sewer/drain backup

Roof claims often hinge on cause of loss + roof condition (and special deductibles may apply)

Next step: Talk to an Agent to sanity-check your policy wording before you assume something is covered.

What you’ll learn

The most common types of home damage that are usually covered

The most common damage types that are usually not covered

The “gray areas” that often depend on endorsements (water backup, mold, code upgrades)

How to review your policy quickly so there are fewer surprises

How does homeowners insurance decide what’s “covered”?

Most homeowners policies follow the same basic logic:

Cause of loss: The event must be covered (or not excluded).

What was damaged: The item must fall under the right coverage bucket (dwelling, other structures, personal property).

Exclusions still apply: Even common losses can be excluded based on circumstances or policy wording.

Deductible and limits: Payment is reduced by your deductible and capped by your limits (and sometimes sublimits).

Rule of thumb: Homeowners insurance is generally built for sudden, accidental events—not maintenance, wear and tear, or long-term predictable problems.

What home damage is usually covered by homeowners insurance?

These categories are often covered on many homeowners policies, but exact coverage depends on your carrier, your policy language, and endorsements.

Fire and smoke damage

House fire damage to the structure

Smoke damage tied to a fire event (coverage varies by circumstance)

Wind and hail damage

Wind damage to roof, siding, fences, and other structures may be covered

Hail damage is often covered, but roof age/condition, materials, and deductibles can matter

Lightning and sudden electrical damage

Lightning strike damage is commonly covered

Some sudden electrical damage may be covered depending on wording and exclusions

Theft and vandalism

Theft after a break-in (often subject to personal property limits/sublimits)

Vandalism or malicious mischief (varies by policy)

Falling objects and sudden impacts

A tree limb falling onto the roof

A vehicle impact into the home (your policy may apply even if another party is responsible)

Weight of ice, snow, or sleet

Some policies cover certain sudden damage tied to the weight of snow/ice, depending on the event and policy terms

Sudden, accidental water damage from inside the home

This is the big one. Many policies often cover sudden accidental discharge like:

Burst pipe

Washing machine hose failure

Water heater rupture

Common “yes, but”: the resulting water damage may be covered, while the failed part (like the worn-out hose) may not be fully covered.

What home damage is usually not covered by homeowners insurance?

These are common exclusions or non-covered situations on many homeowners policies.

Flooding (water coming from outside)

Homeowners insurance typically does not cover flood, such as:

Surface water entering after heavy rain

River/stream overflow

Storm surge

Flood is often handled through a separate flood policy (availability and rules vary).

Earth movement (earthquake, landslide, sinkhole)

Earth movement is commonly excluded and may require a separate policy or endorsement depending on location and carrier.

Wear and tear, deterioration, and maintenance issues

Usually not covered:

An older roof wearing out over time

Rot, corrosion, settling, cracking from age

Deferred maintenance and gradual breakdown

Gradual leaks, repeated seepage, and long-term moisture

Often not covered:

A slow leak under a sink over months

Repeated seepage through foundation

Ongoing humidity issues that lead to damage

Mold (often limited and highly dependent)

Mold coverage is one of the most policy-dependent areas:

Mold tied to a covered sudden water event may have limited coverage

Mold from long-term moisture is often excluded

Pests and infestations

Damage from termites, rodents, insects, and similar issues is usually considered prevention/maintenance and not covered.

Sewer or drain backup (often needs an endorsement)

Backup through sewers or drains is commonly excluded unless you add a water backup (or similar) endorsement.

Intentional damage or neglect

Insurance typically won’t cover damage caused intentionally—or damage that’s made worse by failure to protect the property after a loss.

What are the “gray areas” that depend on endorsements or specifics?

These aren’t “always covered” or “always excluded.” They often come down to policy wording, endorsements, and facts of the loss.

Water: burst pipe vs. flood vs. backup

Burst pipe inside the home: often covered (sudden/accidental)

Flood from outside water: usually not covered (separate policy)

Sewer/drain backup: often endorsement-based

If you’re not sure which bucket your situation falls into, we can help you translate your policy language into plain English.

Roof claims: covered peril vs. roof condition

Wind/hail damage may be covered, but insurers often consider:

Roof age/condition and maintenance

Prior wear and tear vs. a specific storm event

Exclusions, limitations, or special deductibles

Ordinance or law (code upgrade costs)

After a covered loss, bringing the home up to current building code may require optional coverage (often called ordinance or law). Some policies include it automatically; others require an endorsement or higher limit.

Personal property sublimits (jewelry, firearms, collectibles, electronics)

Many policies include special limits for certain categories unless you “schedule” items or add coverage. If you own higher-value items, it’s worth checking.

How can I review my policy quickly (without an insurance degree)?

Pull your declarations page and look for:

Your deductible (and whether wind/hail has a different deductible)

Coverage A (Dwelling), Coverage B (Other Structures), Coverage C (Personal Property)

Any listed sublimits or special limits on certain item types

Whether you have endorsements like water backup or ordinance/law

Any big exclusions called out (flood and earth movement are common examples)

If you want, send a screenshot of your declarations page and we’ll help you spot common gaps—without pressure.

Why work with an independent agency like Silver Harbor Insurance?

Your coverage. Your call.

We lay out your options so you can decide with confidence—across multiple carriers, not just one.

What that looks like in practice:

We help you compare options so you understand what’s covered before a claim

We point out common gaps (like water backup or code upgrade coverage) and show you choices

We’re an online agency—email and our quote form are usually the fastest way to reach us

What to have ready before you talk to an agent

To make the conversation quick and useful, it helps to have:

Your current declarations page (photo/screenshot or PDF)

Your address and basic home details (updates, roof age if known)

Notes on recent improvements (roof, plumbing, electrical, HVAC)

Your preference: lowest premium, lowest surprises, or a balanced approach

A list of higher-value items that might need special handling (if applicable)

Next step: get a plain-English coverage check

If you’re wondering whether your policy would respond to a specific type of damage, we can walk through the “cause of loss” and the endorsements that matter.

Talk to an Agent or Request a Quote—and we’ll help you understand your options with calm, principled guidance.

A Quick Note: We write these articles to help you navigate the complex world of insurance, but they do not replace the expertise of a licensed agent. View this content as a starting point rather than a final word on your specific policy needs. Always talk to a professional to ensure you carry the right protection.

Contact

Quote and support requests 24/7

Phone

© 2026. All rights reserved.