How to choose life insurance for your family: A practical guide

Life insurance doesn't have to be confusing. This guide breaks down the most common options — term and whole — so Utah families can figure out what actually makes sense for their situation, their budget, and the people depending on them.

3/4/2026

Life insurance is one of those topics that makes people want to change the subject. It involves thinking about death, disability, and worst-case scenarios — none of which are fun to contemplate.

But here is the thing: choosing life insurance for your family doesn’t have to be complicated. At its core, life insurance is a financial tool that protects the people you love from financial hardship if something happens to you.

This guide walks through a five-step framework to help you choose the right coverage without the pressure, jargon, or confusion that often comes with the process.

Step 1: Understand why you need coverage

Before you start comparing policies or getting quotes, take a step back and define your “why.” Life insurance means different things to different families, and knowing your reason for buying it will help you choose the right type and amount.

Here are the most common reasons families buy life insurance:

Income replacement: If your paycheck covers the mortgage, groceries, and daily expenses, life insurance ensures that income continues for your family.

Mortgage protection: Your family can stay in their home even without your income.

Education funding: Covering future college tuition or private school costs for your children.

Final expenses: Funeral and burial costs average $7,000–$12,000, a burden many families aren’t prepared for.

Debt payoff: Eliminating credit cards, student loans, or other debts so they don’t pass to your spouse.

Your life stage matters here. A couple in their 30s with young children and a mortgage has very different needs from a 50-year-old whose kids are grown and whose house is almost paid off.

If you are unsure what your family specifically needs, contact us and we can walk through your situation together.

Step 2: Know the difference between term and permanent life insurance

Once you know why you need coverage, you need to understand the two main types of life insurance. The choice between them will shape everything from your monthly cost to how long you’re protected.

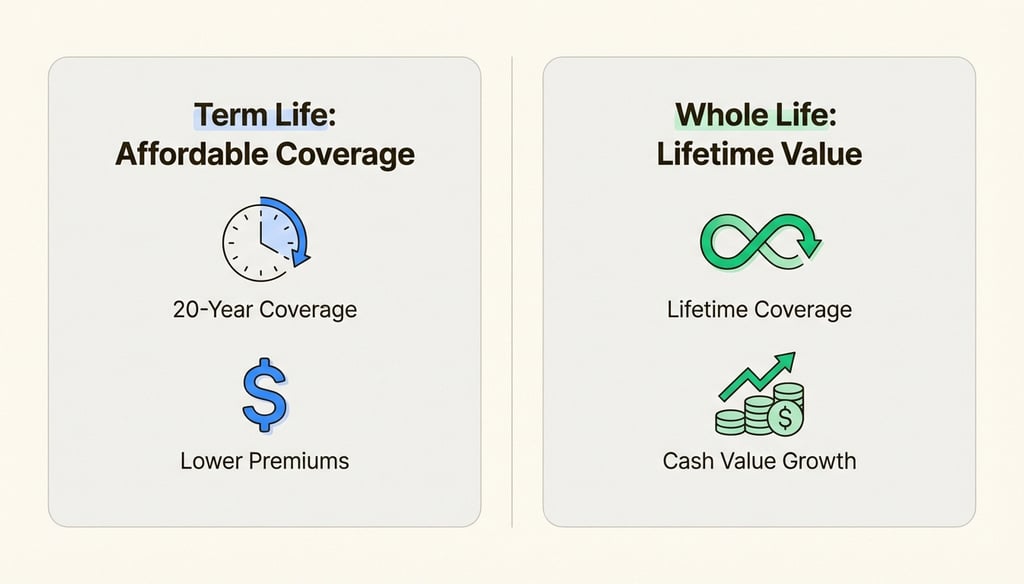

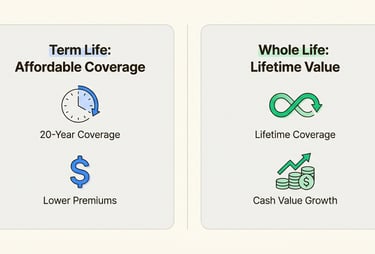

Term life insurance

Term life is straightforward: you buy coverage for a specific period, usually 10, 20, or 30 years. If you die during that period, your beneficiaries receive the death benefit. If you outlive the term, the policy expires.

Why families choose term:

It is the most affordable option

It covers you during the years your family needs protection most (while kids are young, mortgage is active)

Many policies let you convert to permanent coverage later without a new medical exam

Permanent life insurance (whole life)

Whole life policies last your entire lifetime and include a cash value component that grows over time. They are typically more expensive than term, but they serve a different purpose.

Why families choose whole life:

Coverage never expires

Cash value builds as a forced savings mechanism

Useful for estate planning and wealth transfer

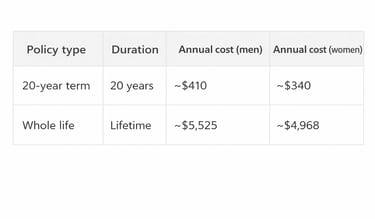

The cost difference

Here is where the rubber meets the road. According to NerdWallet, here is what a healthy 40-year-old might pay for $500,000 in coverage:

That is roughly 13 times more expensive for whole life. For most families, term life makes more sense during the active child-rearing and mortgage-paying years.

The key question to ask yourself: do you need coverage for a specific period (until kids are grown, mortgage is paid off) or for the rest of your life? If you’re not sure, browse our carrier options to see what we offer.

Step 3: Calculate how much coverage you need

This is where many people get stuck. You don’t want to buy too little and leave your family underprotected. But you also don’t want to overbuy and stretch your budget on premiums you can’t sustain.

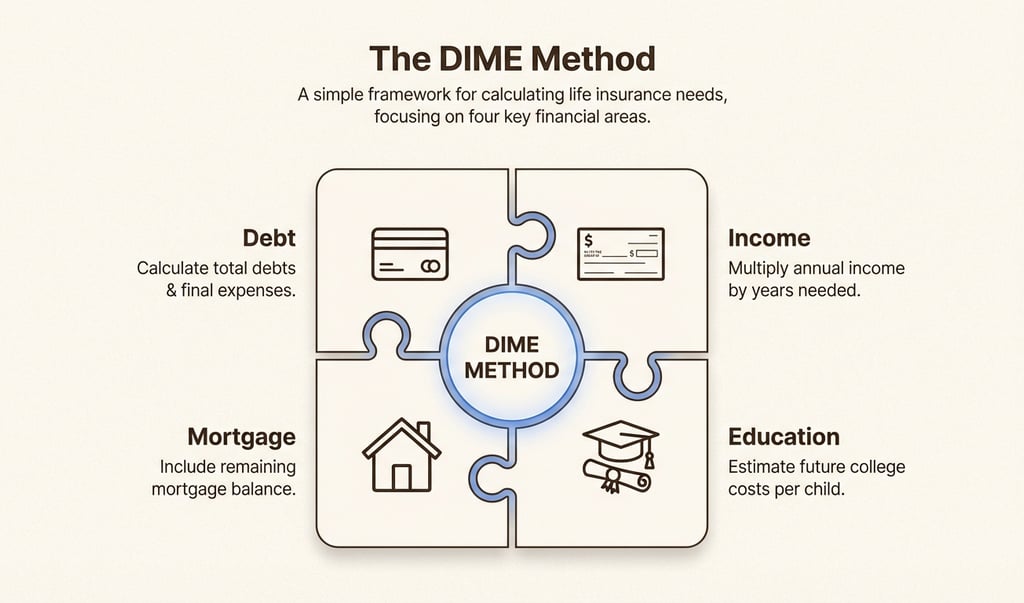

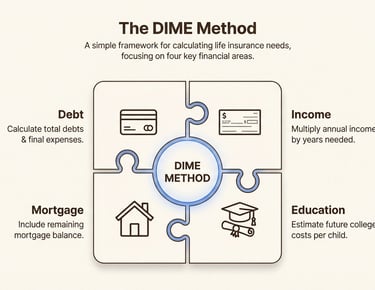

The DIME method

One practical approach is the DIME method, which stands for:

Debt: Total outstanding debts (credit cards, student loans, car loans)

Income: Annual income multiplied by the number of years your family will need support

Mortgage: Remaining balance on your home loan

Education: Estimated future college costs for each child

Add these four numbers together for a solid coverage estimate.

The rule of thumb

If the DIME method feels too detailed, many financial planners recommend a simpler formula: 10 to 15 times your annual income. A parent earning $75,000 per year would aim for $750,000 to $1,125,000 in coverage.

Do not forget stay-at-home parents

Even if one parent doesn’t earn an income, they likely provide significant value through childcare, household management, and other responsibilities. The cost to replace those services (childcare, housekeeping, cooking, etc.) is often $25,000–$50,000 per year.

A quick coverage checklist

When calculating your number, consider:

Mortgage or rent payments remaining

Childcare costs until children are school-age

Daily living expenses (groceries, utilities, transportation)

Outstanding debts beyond the mortgage

Future education expenses

Funeral and final expenses ($7,000–$12,000)

The goal is to replace your income long enough for your family to adjust financially without drastically changing their lifestyle.

Step 4: Choose your beneficiary and policy features

Once you know how much coverage you need, you will make some important decisions about how the policy is structured.

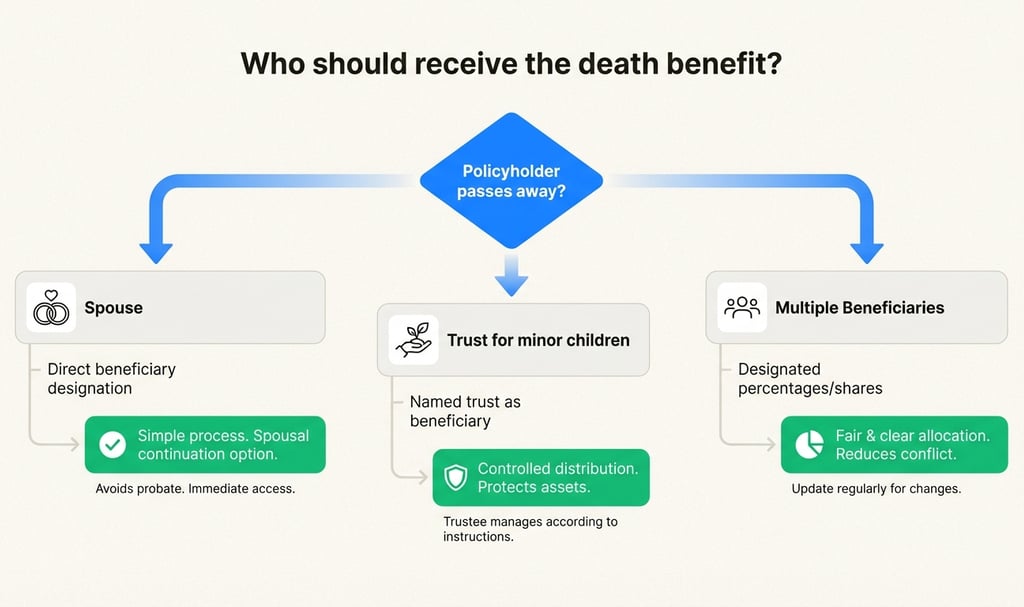

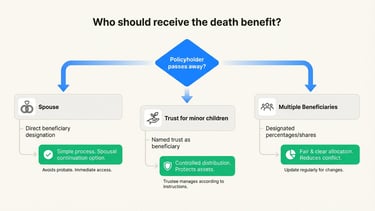

Naming your beneficiary

Your beneficiary is the person (or people) who receive the death benefit. You have several options:

One primary beneficiary: Your spouse receives the full amount

Multiple beneficiaries: Split by percentage (spouse gets 70%, children get 15% each)

Contingent beneficiaries: Backup recipients if the primary beneficiary dies first

A trust: Useful if you have minor children (more on this below)

Important: Don’t name minor children as direct beneficiaries. Insurance companies can’t pay minors directly. Instead, consider setting up a trust or naming a guardian/trustee to manage the funds.

Policy riders to consider

Riders are add-ons that customize your coverage. Some worth considering:

Waiver of premium: If you become disabled and cannot work, the insurance company pays your premiums for you. This is one of the most valuable riders available.

Accelerated death benefit: Allows you to access part of your death benefit if diagnosed with a terminal illness.

Child term rider: Provides a small amount of coverage for your children, usually convertible to their own policy when they reach adulthood.

Spouse rider: Adds term coverage for your spouse to your existing policy.

The convertibility feature

If you buy term life, look for a policy with a convertibility option. This lets you convert your term policy into a whole life policy later — usually without a new medical exam. It’s a valuable feature that keeps your options open.

You don’t have to convert the entire policy. A partial conversion can make sense if you want some permanent coverage but not the full premium commitment.

Step 5: Shop with an independent broker

You have done the hard work of figuring out what you need. Now it is time to find the right policy at the right price — and that means working with the right person.

Captive agents vs. independent brokers

Captive agents work for one insurance company. They can only sell that company’s products, which limits your options.

Independent brokers (like Silver Harbor) work with multiple carriers. They can shop your application across different companies and find the one that rates your risk most favorably.

Why does this matter? Insurance companies rate risk differently. One company might offer you a “preferred” rate while another puts you in a standard category — a difference that can be hundreds of dollars per year.

The application process

Here is what to expect when you apply:

Quote request: Share basic information (age, health, coverage needs) to get estimated rates

Application: Complete a detailed health and lifestyle questionnaire

Medical exam: Many policies require a brief exam (blood draw, urine sample, height/weight check). Some carriers offer no-exam options for lower coverage amounts.

Underwriting: The insurance company reviews your application and medical records

Policy issue: Once approved, you receive your policy documents and pay your first premium

The whole process typically takes 4–6 weeks, though no-exam policies can be faster.

Get coverage while you are healthy

Life insurance gets more expensive every year you wait. Your age and health are the two biggest factors in your premium. A policy that costs $30/month at age 30 might cost $60–$80/month at age 40.

If you have a major health change (diabetes diagnosis, heart condition, etc.), you could find yourself paying significantly higher rates — or being declined altogether.

Have questions about the process? Call us at 801-332-9888 or contact us online. We shop multiple carriers to find your best rate.

Common mistakes to avoid when buying life insurance

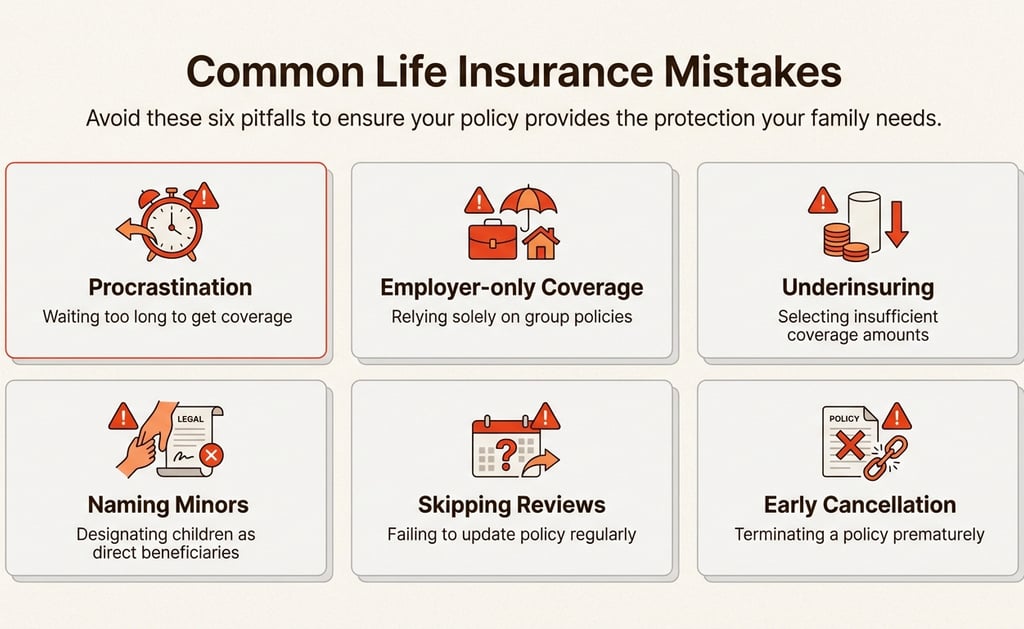

Even with a solid plan, it is easy to make missteps. Here are the most common mistakes we see:

Waiting too long

The number one mistake is procrastination. Every year you wait, premiums increase. A policy that costs $25/month today might cost $45/month in five years.

Relying only on employer coverage

Group life insurance through your job is convenient, but it has limitations. Coverage amounts are often capped at 1–2x your salary, and the policy typically doesn’t follow you if you change jobs.

Underinsuring

A $100,000 policy might sound like a lot, but it won’t go far if you have a mortgage, young children, and a spouse who doesn’t work outside the home.

Naming minors as beneficiaries

As mentioned earlier, insurance companies can’t pay death benefits directly to minors. The court will appoint a conservator to manage the money — a process that adds delays and costs.

Not reviewing coverage after major life events

Your life insurance needs change as your life changes. Get married? Have a child? Buy a house? Each of these events changes your coverage requirements.

Canceling old coverage before new coverage is in force

Never cancel an existing policy until your new policy is fully approved and active. If something goes wrong during the underwriting process, you don’t want to be left without coverage.

Get the right life insurance for your family’s needs

Choosing life insurance isn’t about predicting the future. It’s about preparing for it so your family has options no matter what happens.

Let us recap the five steps:

Understand your why: Define what you are protecting (income, mortgage, education, final expenses)

Know your options: Term life for temporary needs, permanent life for lifelong protection

Calculate your coverage: Use the DIME method or the 10–15x income rule

Structure your policy: Choose beneficiaries wisely and consider valuable riders

Shop smart: Work with an independent broker who can compare multiple carriers

The right policy depends on your unique situation: your age, health, family structure, debts, and financial goals. There is no one-size-fits-all answer — but there is a right answer for your family.

At Silver Harbor Insurance, we lay out your options so you can decide with confidence. We shop multiple carriers, explain the trade-offs, and handle the paperwork. No pressure, no jargon.

Ready to protect your family’s financial future? Contact us anytime — our digital quote system is available 24/7. Or call us directly at 801-332-9888 to speak with an advisor.

Frequently Asked Questions

What is the best way to choose life insurance for your family when you are on a tight budget?

Start with term life insurance. It provides the most coverage for the lowest cost. A healthy 30-year-old can often get $500,000 in coverage for around $25–$30 per month. Focus on getting the right amount of coverage — even if it’s a bare-bones policy — rather than buying a smaller whole life policy that leaves your family underprotected.

How do I choose life insurance for your family if one parent stays at home?

The stay-at-home parent needs coverage too. Consider what it would cost to replace their contributions: childcare, housekeeping, meal prep, transportation, and more. The replacement cost is often $30,000–$50,000 per year, which means the stay-at-home parent needs meaningful coverage despite having no formal income.

Should I choose life insurance for your family through my employer or buy an individual policy?

Employer coverage is a nice benefit but should not be your only protection. Group policies typically offer 1–2x your salary, which is rarely enough. An individual policy that you own and control is portable (it follows you if you change jobs) and usually allows for more coverage.

How often should I review how to choose life insurance for your family as circumstances change?

Review your coverage every 2–3 years and after any major life event: marriage, birth or adoption of a child, home purchase, divorce, or significant income change. A policy that was right five years ago may be inadequate today.

What is the most important factor when you choose life insurance for your family?

The death benefit amount matters most. A policy with the right features but insufficient coverage will fail your family when they need it. After getting the amount right, focus on the insurance company’s financial strength rating (look for A or better from AM Best) and the policy’s specific exclusions.

Can I choose life insurance for your family without taking a medical exam?

Yes, many carriers now offer no-exam policies, though they typically cost more and have lower coverage limits. If you are young and healthy, a fully underwritten policy (with the exam) will almost always give you better rates. If you have health concerns or want a faster approval, no-exam options are worth exploring.

A Quick Note: We write these articles to help you navigate the complex world of insurance, but they do not replace the expertise of a licensed agent. View this content as a starting point rather than a final word on your specific policy needs. Always talk to a professional to ensure you carry the right protection.

Contact

Quote and support requests 24/7

Phone

© 2026. All rights reserved.